Member Content

What Calif.’s top 25 flower brands say about the market

This story has been updated with a statement from Wonderbrett CEO Matt Costa.

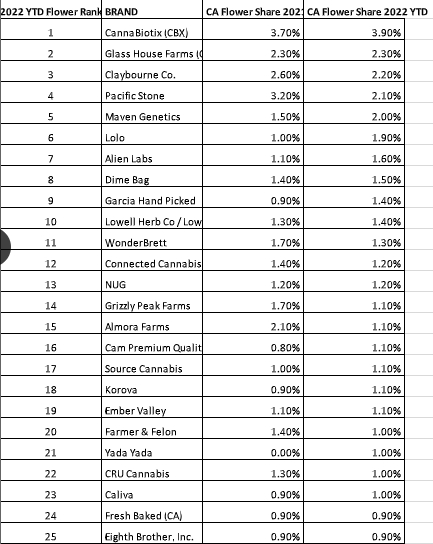

Headset data on California’s highest-grossing flower brands depicts a hypercompetitive market where the 25 bestsellers account for barely one-third of sales. Insiders say the list, shared exclusively with WeedWeek, shows how premium brands are struggling to adapt in the face of improving quality from greenhouse grows and an abundance of inexpensive, high quality product.

Flower’s market share has fallen to about 37% of the total state market but . . .

Log in or become a WeedWeek Member to read this article.